Cyber Attacks on Law Firms Continue

In a recent post, we discussed the growing trend of cyber attacks against law firms. According to a BakerHostetler report based on more than 1,250 incidents across industries, law firm cases nearly doubled from the previous year, driven in part by a threat group that used social engineering tactics—impersonating IT staff, gaining remote access to attorneys’ devices, and quickly stealing sensitive data for ransom. Law firms are especially attractive targets because of the high-value confidential information they hold. A recent lawsuit filed against Fox Rothschild LLP shows the trend is continuing and further highlights the need for broad insurance coverage for cyber attacks.

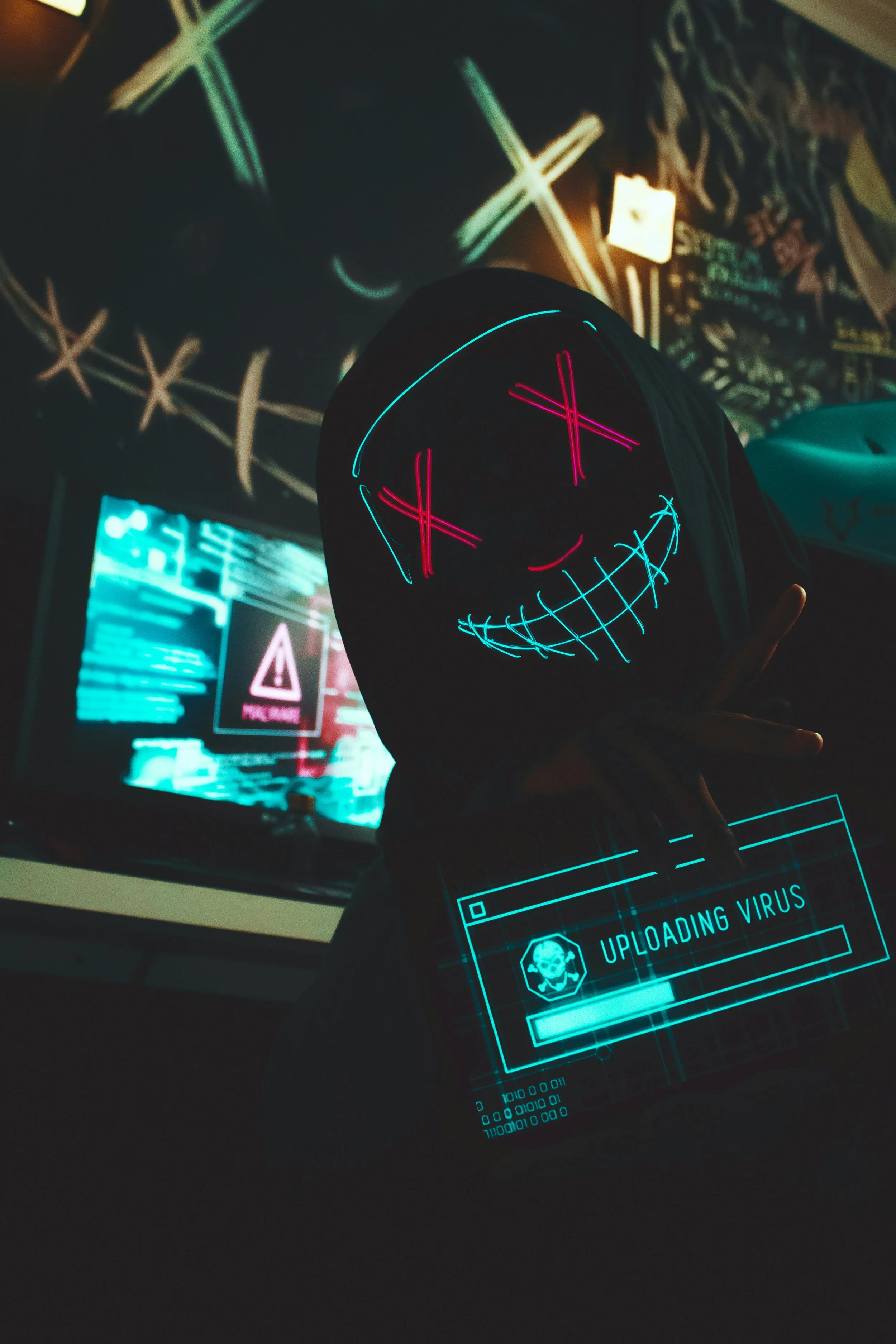

New AI-Enhanced Cyber Attacks Increase Risks for the Uninsured

In recent weeks, the tempo of reporting on cybercriminals’ use of artificial intelligence has only accelerated. What was once speculative commentary about AI-enabled threats has matured into detailed accounts of how threat actors are integrating generative AI into the core of their operations. With these developments, the attacks are both more sophisticated and more frequent, making it more a matter of “when” rather than “if” a business will be victimized. This makes robust Cyber coverage more important than ever.

Cyber Coverage for Ransomware Attacks

Cyber attacks are a serious threat to all businesses and anyone who uses the internet or computer systems. It is a common misconception that cyber attacks prey on those ignorant to cyber operations; however, that is not the case. Anyone can fall prey to the manipulation of cybercrimes because they target the natural tendencies of human behaviors such as taking shortcuts and using quick judgment. Knowing these natural human behaviors, cybercriminals have manipulated human behavior to allow successful cyber attacks. Securing proper cyber insurance policies that cover these kinds of attacks cyber attacks requires careful pursuit of cyber insurance policies in an increasingly resisting market. This is the time to locate specialists in cyber insurance coverage and employ their networks.

What Insurers Do Not Want You to Know About the Policies They Sell

Insurance policies are difficult to read at the best of times. This is a calculated move by the insurance providers in the hopes that policyholders will not avail themselves of all the protections contained therein. On occasion, however, the insurers’ tactics can be turned upon them. The twisting, complicated language can sometimes open the door for policyholders to argue for coverage in areas the insurer may not have intended to provide it. Careful lawyering and receptive judges have codified several of these expanded coverage areas over the years, and a few such examples are presented below.

Are Insurance Policy Applications Traps for the Unwary?

When applying for insurance coverage, the policyholder must complete a policy application. Completing the policy application can be a tedious process containing a number of questions that, to the average person, can seem convoluted and confusing. This is especially the case as policyholders face questions that do not have objective answers. The complicated nature of policy applications raises serious issues where insurers have the ability to rescind the policy contract if the policyholder misrepresents information provided in their policy application.

Why Securing Broad Crime Coverage is the Best Protection Against Cyber-Threats

Our prior blogs have addressed Cyber/Media policies as well as aspects of “social engineering fraud,” one of the most prevalent, problematic, and challenging theft plagues sweeping the country. The best resource against such incidents of Loss is a comprehensive separately secured Crime policy. A recent decision from the Ninth Circuit reversing the district court’s ruling in favor of the policyholder clarified why Crime Policy may be the best to address this risk in Ernst & Haas Management Co. v. Hiscox Inc.

WHAT A CEO NEEDS TO KNOW ABOUT INSURANCE

When is the last time you thought about your company’s insurance coverage? How broad is its scope? How might it address litigation which could arise out of the company’s operations?

Insurance concerns are rarely a priority for CEOs. But, a CEO brings a unique perspective to the oversight of insurance acquisition and use. CEO involvement is inescapable where a Lawsuit becomes an “existential” concern for the Company.

Insurance Recovery for Restitutionary Intellectual Property Claims

Insurance recovery in intellectual property lawsuits is often not limited to “compensatory damages”. Claimants who suffer a Loss in an intellectual property dispute may secure recovery that is not limited to “compensatory damages”. Licensing revenue is commonly recoverable in the successful pursuit of trademark infringement lawsuits.

Coverage for Malware Attacks – Crytpojacking and Ransomware

With malware attacks on the rise and evolving, policyholders need to secure proper cyber insurance coverage to protect them against the costly expenses of these attacks.

Insurance Coverage for and IT Consultant’s Role in Media/Cyber Policy Application

As many entities shift a number of employees to remote desktop work, policyholders face the challenge of procuring appropriate coverage for risks arising from their growing online business operations. Traditional policies leave gaps in coverage for cyber-related claims as their policy language rarely include the necessary protections for injury cause through online operations. Make sure you have the appropriate coverage for your online business by securing Cyber/Media polices into your insurance portfolio.

Reach for the Stick: Why Dynamite is Less Dangerous Than "Claims Made & Reported" Policies

Dynamite is inherently risky and should be treated with kid gloves. Nitroglycerin, an element, within the dynamite is susceptible to shock and so must be handled with extreme caution and care. Compared to dynamite, “Claims-Made-and-Reported” policies include a number of traps for the unwary policyholder that if not mindful can result in major losses.

Conservative 5th Circuit Broadly Construes "Publication" in Policy to Cover Hack

Despite generally analogous insurance policies being available across the country, the location of a lawsuit and the predispositions of particular courts can often be determining factors in coverage lawsuits, particularly where a case comes down to conventions of policy interpretation.

Avoiding Malpractice by Providing Prompt Notice of Intellectual Property Claims to Insurers

“Intellectual property attorneys may have a duty to apprize their clients of the need to notify their clients’ insurers of claims as part of their retention in order to fully represent their clients’ interests in a lawsuit for which they are counsel of record.”